Tag: Tax season (page 2 of 3)

If you installed a solar panel system or another type of renewable energy system during 2023 to your home, you may be eligible for a tax credit which would be equal to around 30% of the total cost of installation.

If you purchased a new qualified plug-in electric vehicle that is less than 4,000 pounds and has a battery of at least 4 kilowatt-hours, you may be eligible for a tax credit up to $7,500 per vehicle!

Starting with tax year 2023, if your business has 10 or more W2s and/or 1099s to prepare, you must file them electronically with the IRS.

Get a jump start on next year’s return! The government is constantly coming out with new ways to save on taxes every year. This year the best ways to do so involve energy home savings and electric cars which you can find below:

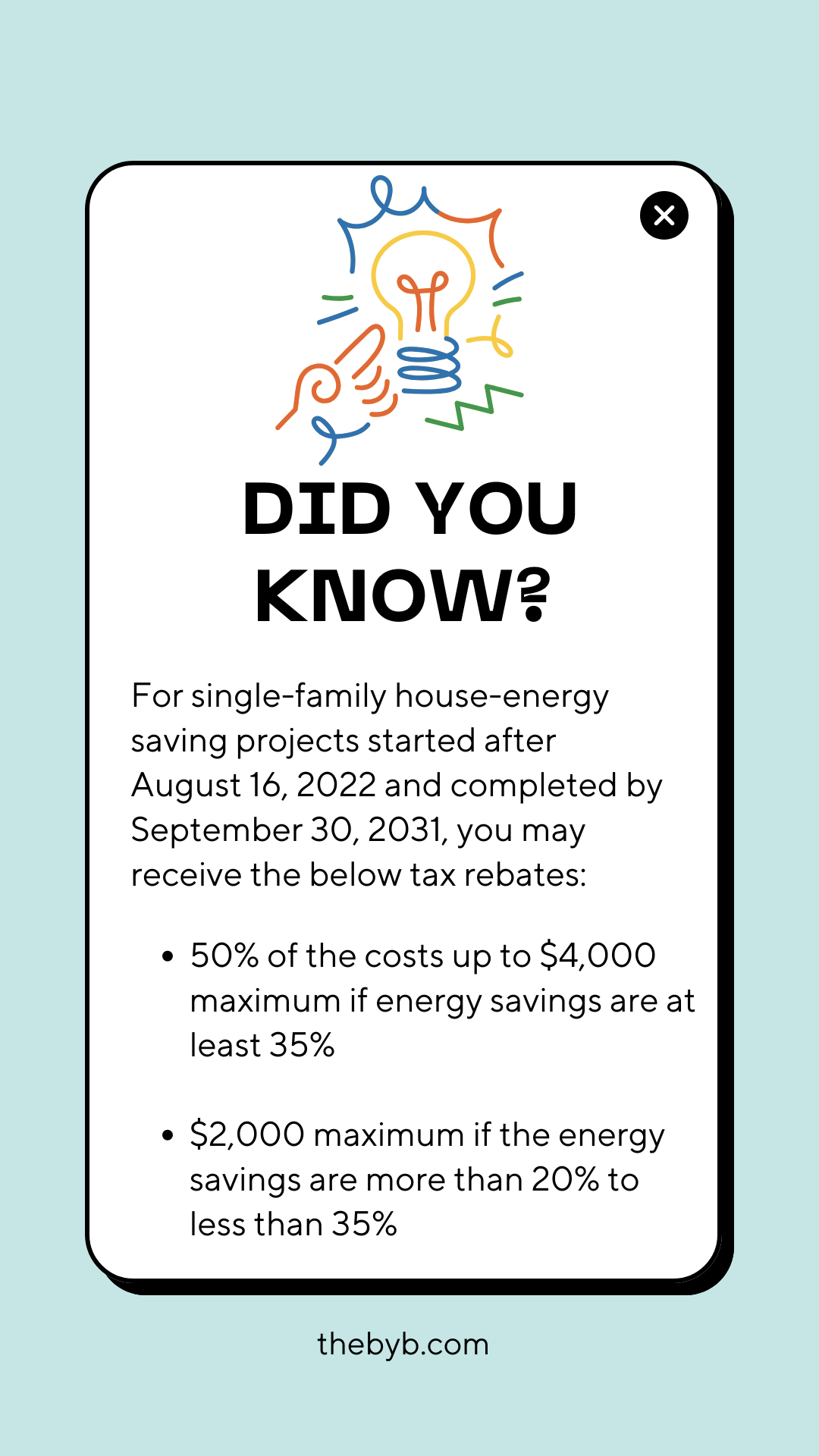

1) For single-family house-energy savings projects started after August 16, 2022 and that will be completed by September 30, 2031, you may receive the below rebates:

– 50% of the costs up to $4000 maximum if energy savings are at least 35%

– $2000 maximum if the energy savings are more than 20% to less than 35%

2) For new construction of energy saving appliances, the following maximum rebates can be achieved:

– $1750 for a heat pump water heater

– $8000 for a heat pump for space heating or cooling

– $840 for either an electric stove, oven, etc. or an electric heat pump clothes dryer

–

3) For new construction of non-appliance upgrades, the following maximum rebates can be achieved:

– $4000 for an electric load service center upgrade

– $1600 for insulation, air sealing, and ventilation

– $2500 for electric wiring

–

4) The Clean Vehicle Tax Credit – this is a $7500 credit for yourself if you:

– buy a new electric vehicle that has final assembly in North America

– is a four-wheel vehicle and is for use on public streets

– has a minimum battery capacity of 7 kilowatt-hours

– does not exceed $80,000 for vans, SUVs, and pick-ups and $55,000 for other vehicles

To achieve the above credit, your adjusted gross income (AGI) must not exceed:

$300,000 for Married Filing Jointly

$225,000 for Head of Household

$150,000 for all others

© 2025 Business of Your Business

Theme by Anders Noren — Up ↑