Tag: Tax season (page 2 of 4)

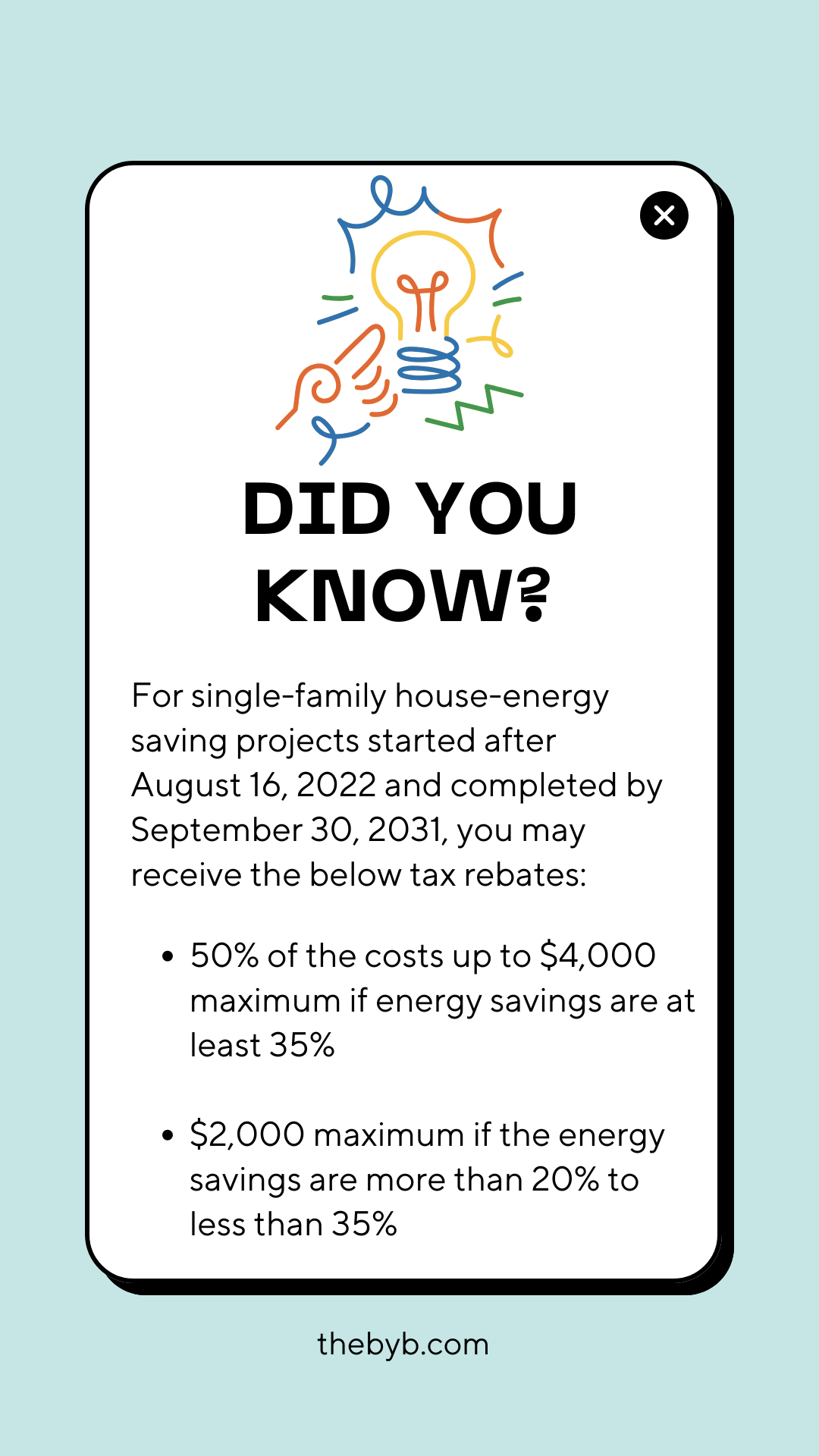

If you installed a solar panel system or another type of renewable energy system during 2023 to your home, you may be eligible for a tax credit which would be equal to around 30% of the total cost of installation.

If you purchased a new qualified plug-in electric vehicle that is less than 4,000 pounds and has a battery of at least 4 kilowatt-hours, you may be eligible for a tax credit up to $7,500 per vehicle!

© 2025 Business of Your Business

Theme by Anders Noren — Up ↑